Why options skew matters for real portfolios

When people first hear про “skew”, it sounds like a math trick only quants care about. In reality, options skew is one of the few pieces of market data that quietly tells you where traders expect pain to show up and how scared they are of big moves. If you just buy or sell options by looking at “cheap” or “expensive” premium without reading the skew, you’re flying blind. For someone trying to reduce concentration risk in a portfolio full of tech stocks, bank shares or crypto‑related names, ignoring skew is like ignoring the weather forecast before sailing: you might be fine, but when the storm hits, it’s going to feel very personal and very expensive.

Clear definitions: skew, concentration risk, diversification

Let’s pin down a few terms before diving into options skew trading strategies. “Implied volatility” is the volatility level backed out from option prices; it’s the market’s consensus about how wild moves might get. “Skew” (or volatility skew / smile) describes how implied volatility changes across strikes: usually out‑of‑the‑money puts trade with higher implied vol than at‑the‑money options, because people fear crashes more than rallies. “Concentration risk” is the danger that too much of your wealth depends on one stock, one sector, one factor or even one country. Finally, “portfolio diversification with options” means using calls, puts and spreads to reshape your payoff profile so that a hit to one position doesn’t wreck your entire capital curve.

Text‑based diagram: how skew is usually shaped

Picture the horizontal axis as strike price, and the vertical axis as implied volatility. A very simplified diagram for a typical equity index might look like this in text form:

Strike: low ←——— ATM ——→ high

Vol: high __

__ medium

___ low

In words, as you move from very low strikes (deep out‑of‑the‑money puts) toward the at‑the‑money point, implied volatility falls, then flattens or dips slightly as you go to high strikes. This downward‑sloping line is the skew. When you’re choosing how to hedge concentration risk with options, you’re really deciding where on this skew you want to pay up for insurance and where you’re willing to be a seller of fear.

How skew links to concentration risk in practice

Imagine your portfolio is 70% concentrated in one growth stock and a couple of its close competitors. You’re not just exposed to that ticker; you’re tied to the same theme, same factor, same news cycle. If something hits that business model, everything sinks together. Skew enters the picture because the market typically overpays for crash protection in those names after big rallies, which means your insurance gets more expensive exactly when you start to feel nervous. Understanding this, you can design the best options strategies for risk management that lean into selling certain overpriced wings while still holding onto the crash protection you genuinely need, reducing net cost without leaving yourself naked in a disaster scenario.

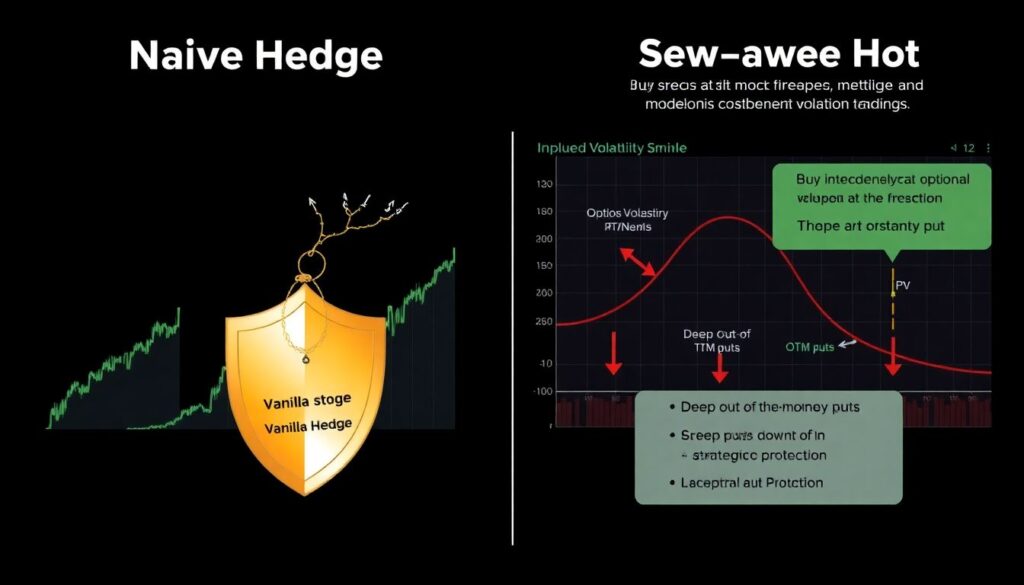

Comparing simple hedging vs skew‑aware hedging

Many beginners start with a naive hedge: buy some at‑the‑money puts on their favorite stock and hope that’s enough. This “vanilla hedge” is easy to understand but often overpriced, especially after volatility spikes. A skew‑aware hedge works differently: you notice that deep out‑of‑the‑money puts are extremely expensive on a volatility basis compared with slightly out‑of‑the‑money ones, so instead of blindly buying the deepest protection, you might buy a slightly out‑of‑the‑money put and partially fund it by selling a further‑out‑of‑the‑money put or a call where skew is flatter. Diagrammatically, you’re sliding your protection along the curve where every unit of premium buys the most expected risk reduction, instead of just grabbing whatever looks scariest.

Common rookie mistakes when using options to “diversify”

New traders often confuse activity with risk control. A classic error is buying loads of weekly options on the same stock they’re already concentrated in, thinking this provides diversification. In reality, they’ve doubled down on the same risk, just with more leverage and faster time decay. Another frequent mistake is ignoring correlation and only looking at ticker symbols: they might own several different tech names and then buy index puts on that same tech‑heavy index, which mostly hedge what they already have, while leaving other portfolio chunks exposed. A more subtle error appears in options skew trading strategies: beginners sell options where the skew is rich without stress‑testing what happens in a tail event, so they pocket tiny premiums for months and then lose years of gains in one shocked move.

Misreading “cheap” and “expensive” options

Another beginner trap is to treat low implied volatility as “cheap” and high implied volatility as “expensive” without context. Suppose skew is very steep in downside puts: they’re high vol, sure, but that may reflect realistic crash risk. Selling them because “the vol is huge” can turn you into involuntary catastrophe insurance. Conversely, slightly out‑of‑the‑money calls on a crowded momentum stock might look cheap in volatility terms, but they can be structurally overpriced relative to the realistic probability of further big upside. When you use portfolio diversification with options, your goal is not to find the absolute cheapest premium but to find options priced attractively relative to the protection or convexity they add to your whole portfolio, after you account for skew and correlation.

Building a skew‑aware diversified options overlay

To weave options into your portfolio in a smarter way, start from the top down. First, identify your true concentrations: sectors, styles, currencies, even specific macro themes like “rates stay low” or “oil remains cheap”. Next, map which indices or liquid large‑caps best represent those risks. Now you can think about how to hedge concentration risk with options by buying protection on the broad proxy rather than just the individual stock. Skew helps here: index puts may have a different skew shape than the single names, sometimes offering cheaper crash insurance per unit of risk reduced. In text‑diagram form, you might see a steep skew line for your favorite stock, but a smoother skew for the index, and that difference can save significant premium when constructing your overlay.

Example: single‑stock heavy bag vs index‑based hedge

Say you hold a big position in a high‑beta chipmaker plus several other semiconductor names. Instead of buying expensive deep puts on each name, you could buy slightly out‑of‑the‑money puts on the semiconductor sector ETF, where skew might be less extreme. To offset cost, you might sell covered calls on the individual names at strikes where upside skew is relatively rich. Functionally, you’re transferring some idiosyncratic upside into broad downside protection: giving up a bit of speculative win potential to meaningfully cut your worst‑case drawdown. This is a concrete use of options skew trading strategies: sell where the market overpays for tails you’re willing to truncate, buy where the market underestimates the pain you absolutely cannot afford.

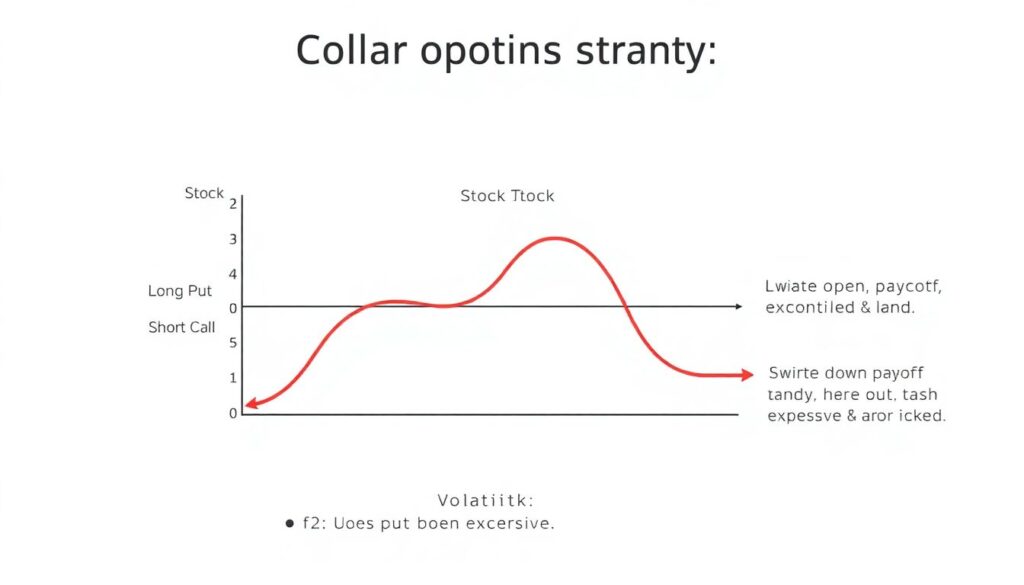

Risk‑managed use of spreads, collars and ratio structures

Most people first meet options via naked calls or puts, but for actual portfolios, spreads and collars are usually safer and more predictable. A collar — long stock, long put, short call — turns a wide open payoff into a controlled band. Skew is your friend here: because downside puts are more expensive, the call you sell may not fully fund your put, but by choosing strikes intelligently you can find a compromise where the premium outlay is modest and your worst loss is capped at a level you can stomach. Vertical spreads also lean on skew: buying a put at a strike with relatively fair vol and selling another where vol is even richer lets you lock in crash protection at a discount to outright puts, while still sharply reducing concentration risk in drawdown scenarios.

What goes wrong when beginners misuse spreads

Rookies often hear that spreads are “safer” and then overbuild complex structures they don’t really understand. They might run ratio spreads — for instance, buying one put and selling two lower‑strike puts — because they see a credit and assume they’ve hacked the system. The hidden catch is that if the underlying crashes through both strikes, they’re now net short optionality in the most dangerous region of the skew. That’s how someone trying to be conservative ends up long a concentrated stock and short a pile of deep out‑of‑the‑money crash protection at the exact moment everyone else is desperate to buy it. To avoid this, treat any structure that leaves you short more contracts than you’re long as advanced, and stress‑test it against extreme but plausible moves before you even think about executing it.

When to consider professional risk management help

If your portfolio is large relative to your income or business, treating risk management as a part‑time hobby can be costly. This is where options risk management services for investors come in. Professional desks and advisors look at your holdings, measure correlations and factor exposures, and then design an overlay that exploits skew instead of getting steamrolled by it. They may, for example, ladder index puts across strikes where skew is favorable, finance them with call overwriting on diversified baskets rather than on your single most beloved name, and keep the structures consistent over time instead of panic‑buying protection after every scary headline. Even if you prefer a do‑it‑yourself approach, studying how these services structure trades can keep your own experiments grounded in sound risk logic.

How to learn without blowing up your account

The best way to integrate options into your diversification plan is to start small and treat each position as a lesson. Before placing a trade, sketch a text‑based payoff diagram for various scenarios: big rally, mild drift, sharp selloff, total crash. Ask yourself who is on the other side of your trade and why they might be happy to take it. Keep a simple log: which skew shape you saw, what role the option plays in the portfolio, and how it behaved when volatility moved. Over time you’ll notice patterns: some “cheap” calls never pay, some “expensive” puts feel worth every cent in a nasty week. Use those observations to refine your personal list of best options strategies for risk management, and keep your position sizes small enough that mistakes become tuition, not bankruptcy.