Skew as a Market Sentiment Gauge: A Practical Introduction

Historical background

From textbook symmetry to real‑world fear

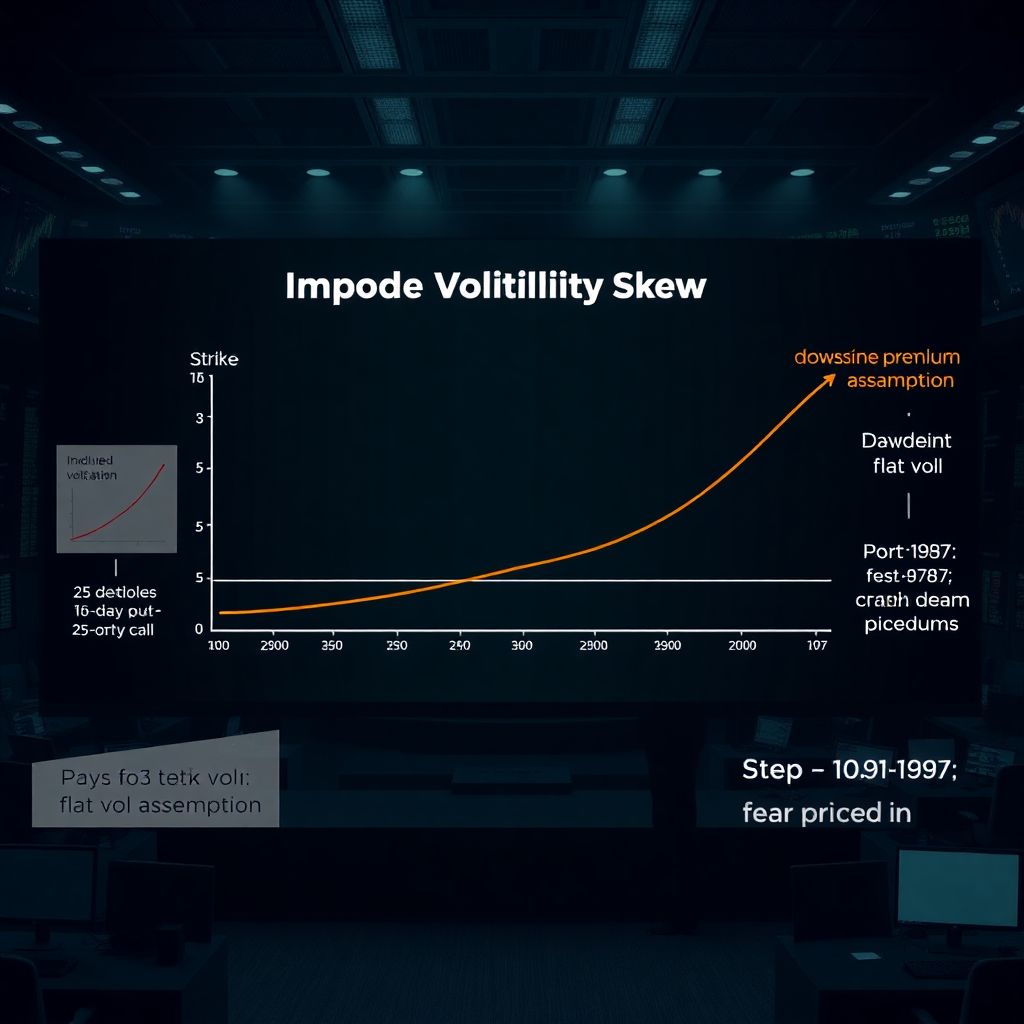

In the original Black–Scholes world, implied volatility was supposed to be flat: every strike, same vol, nice smooth curve. Then 1987 happened, and the market basically said, “Yeah, no.” Index options started to price crash risk much higher than upside, and the volatility “smile” morphed into a downside “smirk”. That was the birth of modern skew as we use it today. Instead of treating options as abstract math objects, traders began to read skew as a direct reflection of crowd psychology: fear of crashes, demand for protection, and willingness to pay for upside. Over the 1990s and 2000s, dealers and hedge funds systematized this intuition, turning skew into a de‑facto barometer of risk appetite, especially in equity indices and FX.

Skew indices like the Cboe SKEW and various bank‑built measures emerged as shortcuts: one number summarizing how much more investors fear big downside moves than big upside ones.

Why skew survived every regime change

Despite changing volatility regimes, zero rates and meme stocks, the basic idea stuck: when people are scared, they overpay for puts; when they’re greedy, they chase calls. Skew condensed that behavior into an observable, tradeable pattern.

Basic principles

What skew actually measures

At its core, skew is just the shape of implied volatility across strikes. If you plot strike on the x‑axis and implied vol on the y‑axis, the curve is your volatility surface slice; the slope and curvature are the skew. For equity indices, downside puts usually trade at higher vols than at‑the‑money options, and upside calls at lower vols. That’s your “downside skew”. This asymmetry is where the phrase options skew market sentiment comes from: the curve encodes how much more the market fears a crash versus a melt‑up. Quant desks often summarize it using simple metrics: the vol of a 25‑delta put minus the vol of a 25‑delta call, or the regression slope of vol versus moneyness. You don’t need fancy math to use it, but you do need to know which point on the curve you’re talking about.

Think of skew as an insurance market: higher downside vols mean protection is expensive, not just in absolute terms but relative to upside.

Reading skew intraday like a trader

Day to day, traders don’t obsess over the full surface; they watch where new risk is being priced. Are out‑of‑the‑money puts suddenly bid while the index barely moves? Skew is steepening and protection is being hoarded.

They also watch whether calls “catch a bid” into rallies. When upside vols rise relative to puts, that’s often a sentiment shift from fear to FOMO, especially around single‑stock news.

How skew ties into sentiment and order flow

Once you see skew as supply and demand for specific tails, the sentiment angle becomes clear. A steep downside skew often indicates structural protection buyers: pensions, asset managers, macro funds trying to hedge equity or credit risk. If that demand intensifies without a matching move in spot, it’s usually a sign of quiet anxiety building under the surface. Conversely, in exuberant markets, you sometimes see “smiley” skew in certain names: both downside and far‑out‑of‑the‑money calls trade rich, because traders crave convexity in both directions. This is where the put call skew indicator trading logic comes in: you’re not just looking at one strike, you’re comparing how the crowd prices bad outcomes versus spectacular ones. Importantly, skew can be regime‑dependent. In FX, for instance, some pairs spend long periods with positive call skew because the market fears a sharp appreciation rather than depreciation, reflecting macro imbalances and carry dynamics.

So the same numerical skew in two assets can mean very different things; context and macro backdrop matter more than the raw value.

How to use skew for practical sentiment analysis

If you’re wondering how to use options skew for sentiment analysis, think in relative rather than absolute terms. First, compare today’s skew to its own recent history: is downside vol exceptionally rich versus the last three to six months? That often signals elevated crash hedging, even if spot volatility is muted. Second, compare skew across related instruments: if S&P skew spikes while sector ETFs lag, hedging is concentrated in the benchmark rather than in single names. That can hint at top‑down macro fear instead of idiosyncratic worries. Finally, connect skew shifts to events: before earnings, a sharp steepening in downside versus upside can indicate that investors are far more afraid of disappointment than excited about a beat, which is informational even if you never touch an option.

In practice, you’re looking for divergences: sentiment implied by skew that doesn’t line up with the narrative in headlines or price action.

Implementation examples

Case 1: Index hedging and skew as warning light

Consider a real‑world pattern from 2018 in the S&P 500. A mid‑sized European asset manager ran a systematic skew index trading strategy as an overlay to its equity portfolio. Each week, they compared the implied vol of 10–15% OTM puts to ATM vols. Whenever that ratio broke above the 90th percentile of its one‑year range, they treated it as a “stress signal”, regardless of what realized volatility was doing. In January 2018, while spot kept grinding higher, their skew signal triggered: deep OTM puts were being hoarded, and downside vol richened aggressively. They responded by trimming net equity exposure and layering in cheap calendar spread hedges. When the “volmageddon” spike hit in early February, their drawdown was about half of their benchmark peers. The key wasn’t predicting the exact timing; it was respecting the message from protection markets, which had started to reprice tail risk well before spot cracked.

Notice they didn’t mechanically short skew; instead, they used it as a risk dial to adjust exposure size and hedge intensity.

Takeaway from the 2018 case

The lesson is simple: skew often moves first, price second. If you wait for the index to sell off before believing the options market, you’re usually late.

Case 2: Single‑stock earnings and upside panic

Another example: a US long/short equity fund trading a mega‑cap tech name into earnings. Historically, this stock showed stable downside‑heavy skew: puts rich, calls cheap. In one quarter, though, something odd appeared in the options skew data for retail traders tracking the name: far OTM calls, 10–15% above spot, suddenly traded at elevated implied vols days before earnings. Retail flow on zero‑day and weekly calls surged, and market makers had to buy stock to hedge, feeding into a pre‑earnings ramp. The fund’s options desk interpreted this as sentiment overheating on the upside: instead of buying calls, they sold call spreads and used the premium to finance slightly OTM puts. Earnings came in solid but not spectacular, the stock popped briefly then mean‑reverted. Upside vols collapsed, skew normalized, and their structure profited from both the vol crush and light downside follow‑through. Skew wasn’t about predicting earnings; it was about reading positioning and crowd expectations around the event.

Here, upside‑rich skew spoke of speculative enthusiasm, not fear; trading against that exuberance proved more efficient than guessing the EPS number.

Case 3: FX crisis premium vs equity complacency

A macro hedge fund once spotted a disconnect: EM FX options priced massive downside skew, while the corresponding EM equity ETF showed relatively tame skew. Currency traders were hedging a crisis; equity investors were still relaxed. The fund concluded that if stress escalated, equity skew would have to “catch up”. They bought cheap downside equity skew via put spreads while partially hedging FX, betting on convergence of sentiment between the two markets. A few weeks later, local political turmoil intensified, equities gapped lower and ETF skew steepened sharply as latecomers rushed for protection. The fund monetized the richened equity puts and rolled some profits into FX structures. Again, skew was a cross‑asset sentiment mismatch rather than a standalone timing tool.

When two markets tell different stories about risk, the one with richer history of pricing crises is often the one to trust.

Common misconceptions

Skew is not a crystal ball or a trade by itself

One of the most persistent myths is that skew directly predicts future direction or that a high SKEW index guarantees an imminent crash. In reality, skew measures how much people are paying for particular tails today, not what will actually happen tomorrow. You can have persistently steep downside skew and a grinding bull market for months. That’s why professional desks rarely use skew in isolation; they treat it as one lens among many: realized volatility, term structure, dealer gamma positioning, and macro data. Another misunderstanding is that rising skew always equals fear. Sometimes, regulatory or structural changes (like new structured product issuance) distort the surface independently of sentiment. For example, heavy issuance of autocallable notes in Asia can systematically steepen or flatten skew in certain indices, because dealers hedge those products in specific strikes. If you ignore such supply‑demand mechanics, you’ll misread the signal and think “fear” where there’s just structured flow.

So the healthy mindset is: skew tells you what insurance costs and who might be buying or selling it, not what the future must look like.

Retail access and overfitting the signal

Another misconception is that skew is only for big banks. In reality, most modern broker platforms provide at least basic skew charts or raw implied vols by strike, making it perfectly possible to incorporate options skew data for retail traders into a workflow. The trap is overfitting: building complicated rules like “if 25‑delta put vol minus call vol exceeds X, then short the index” without testing across regimes and markets. Skew relationships are noisy, and transaction costs plus slippage can eat theoretical edges. A more realistic approach for non‑institutional traders is to treat skew as a context filter: for example, be more cautious with directional longs when downside skew is at extremes, or prefer spreads that sell expensive tails and buy cheaper ones, rather than naked options. Used this way, skew enhances risk management rather than replacing it with a magic formula.

In other words, skew is best as a sanity‑check and structuring tool, not as a standalone signal generator.

Practical tips for everyday use

To wrap this up, treat skew like you would credit spreads or volatility indices: a continuous readout of collective anxiety and greed, not a red‑green traffic light. First, anchor yourself: know what “normal” skew looks like for your asset, both in level and shape. Second, track changes around catalysts: FOMC, earnings, macro data. Often the shift in skew tells you more about how people are positioned than the move in spot. Third, translate the observation into structure choice: rich downside? Maybe express bullish views with put spreads instead of calls. Flat skew and cheap upside? Call diagonals or flies might be better. That’s the essence of a sane skew index trading strategy for non‑quants: use skew to fine‑tune how you take risk, not whether you take it. When you approach skew this way, you move from passively accepting market prices to actively deciding which parts of the distribution you’re willing to own or sell.

Over time, this habit builds a much more nuanced sense of market sentiment than any single headline or chart can provide.